09/04/2026

EU sustainability reporting coverage varies widely across industrial sectors

EU’s CSRD directive made sustainability reporting a legal obligation for a large number of companies. It requires them to publicly disclose how their operations affect the environment and people, and how environmental risks affect them in return. A closer look reveals that the directive does not reach all industries equally – not even within heavy industry.

The CSRD entered into force in 2023, with the aim of producing comparable data on companies’ environmental and social impacts. This gives investors, financiers, and other stakeholders the information they need to make informed decisions. Yet before the first reports had even been published, the directive began to be scaled back through the Omnibus reform*. This shifted the debate to a single number: around 80 percent of previously in-scope companies will fall out of scope.

Turnover, not company counts

The Commission justifies the narrower scope by arguing that the remaining companies are most likely those with the greatest impacts on people and the environment. Also, it is assumed that the largest companies account for the bulk of turnover. But does this assumption hold equally across all industries?

The difference in coverage between service sectors and industry has drawn some public attention, but how coverage varies across industrial subsectors has gone largely unnoticed. Yet mining, water and waste management, manufacturing, energy, and construction differ significantly in their corporate structures.

How well does CSRD reach different industries?

Using Eurostat business statistics, I looked at two scenarios across those industrial sectors: coverage under the original CSRD and coverage after the Omnibus.

I calculated the original CSRD coverage by comparing the combined turnover of companies subject to the reporting obligation with the total turnover of each industrial sector. The figure is based solely on the headcount criterion, but broadly reflects reality. The Omnibus figures are rough estimates, as data was limited.

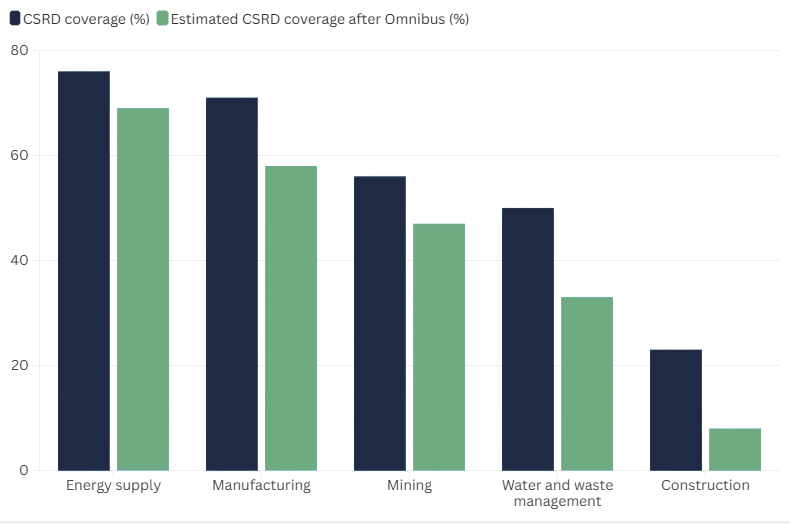

In energy supply, three-quarters of turnover falls within CSRD reporting scope; in construction, less than a quarter.** Data from 2024. Source: Eurostat, SBS

Energy and manufacturing have the highest CSRD coverage

According to this analysis, coverage is highest in energy supply: there the vast majority of turnover comes from companies subject to reporting obligations. The sector is capital-intensive, as electricity and gas production requires massive investment, which favors large players.

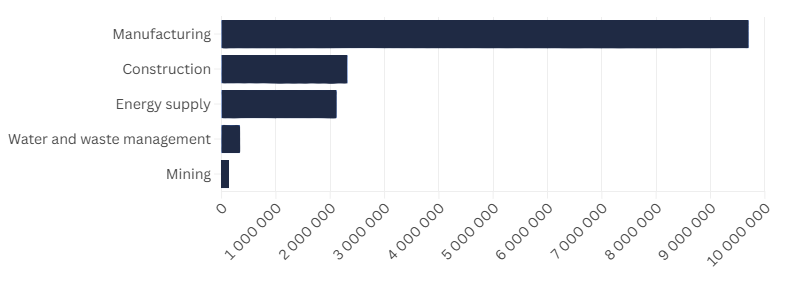

Manufacturing follows close behind. Large automotive, chemical, and electronics groups generate the bulk of the sector’s turnover. However, total sector turnover approaches €10 trillion, so even a modest unreported share translates into a substantial sum in absolute terms.

Total turnover of industrial sectors in millions of euros, 2024.

Source: Eurostat, SBS

Construction falls furthest into the blind spot

Construction stands out clearly in the data: the CSRD reaches only a small share of construction sector turnover. This is no surprise in a sector where output is distributed across small firms and long subcontracting chains.

This structure is precisely what makes sustainability monitoring particularly difficult: the longer the chain, the less visibility the main contractor has over how work is actually carried out at the end of it. Fragmentation is thus both a statistical problem and a structural barrier to sustainability.

The CSRD reaches sectors that are already regulated

Large companies in the energy and process industries, which typically fall under the EU Emissions Trading System and the Industrial Emissions Directive, easily exceed the CSRD threshold. The CSRD thus layers obligations onto sectors that are already regulated.

Construction shows the opposite: the CSRD covers only a fraction of sector revenue, while environmental regulation is also more fragmented. This refers to a regulatory gap, and the Omnibus proposal will likely widen it further.

Reporting can only support decision-making if the data is of good quality and there is a will to use it – among investors, financiers, and companies.

Coverage is only part of the picture

It is worth remembering that sustainability reporting is not a goal but a tool. Reporting can only support decision-making if the data is of good quality and there is a will to use it – among investors, financiers, and companies.

Also, smaller companies are not entirely outside the system, as reporting obligations flow down from large companies to their suppliers. In fragmented sectors, however, supply chain pressure is likely to carry less weight. This means sustainability data will depend almost entirely on large companies.

* The original CSRD criteria cover listed companies and companies meeting at least two of three thresholds: more than 250 employees, turnover above €40 million, or a balance sheet above €20 million. Following the Omnibus, the reporting obligation applies to companies with more than 1,000 employees and a turnover exceeding €450 million.

** In mining and water and waste management, companies can have large turnovers and balance sheets with relatively few employees, so an analysis based on the headcount criterion alone may underestimate their true coverage.

Want to know more?

Dismantling sustainability regulation is self-defeating

The sustainability crisis is a complex phenomenon marked by both serious global challenges and encouraging progress. In recent years, we have seen plenty of both. Now, concern is mounting over the so-called Omnibus initiative, which threatens to undermine the quality of sustainability reporting. Especially troubling is its disregard for value chain analysis – even though some of the most significant sustainability impacts occur precisely within those chains.

Visionary – Katrin Keis

Nomine Consult, a frontrunner in energy and environmental consulting, joined Elomatic in spring 2025. We sat down with Katrin Keis, head of Nomine Consult’s Estonia office and lead of their environmental and sustainability services, to discuss the evolving role of consultants and the power of networking.